Financing your new car and understanding the cost of ownership

In the U.S., the average cost of a brand-new car is over $36,000. That’s a mountain of moolah–far more than many consumers can pay outright, even with help from a trade-in. Factor in the other costs of ownership, and you’re looking at massive financial commitment. Let’s make sure you can afford it.

A checklist for loans

If you’re planing to take out an auto loan, you might be tempted to do so through your local dealership. It’s advertising low, low rates and other incentives, so surely it’s the best deal in town, right?

If you’re planing to take out an auto loan, you might be tempted to do so through your local dealership. It’s advertising low, low rates and other incentives, so surely it’s the best deal in town, right?

Maybe–but then again, maybe not. You’ll never know unless you do your homework.

Before you sign on the dotted line, investigate auto loans from other sources like banks and credit unions. You might also visit a site like LendingTree.com, where you can receive loan offers from lots of different sources with one fairly simple application. (Just be prepare for plenty of spam afterward. Ugh.)

Wherever you go, make sure the lender isn’t pulling a hard credit inquiry–not yet, anyway. Hard inquiries remain on your credit report for up to two years and can bring down your credit score, which is obviously something you don’t want to do when you’re searching for a loan. Most reputable companies will just run a quick, soft inquiry to pre-qualify you for a loan. They won’t run a hard inquiry unless you authorize it, which you shouldn’t do unless you’re really sure that you’ve found the lowest possible interest rate.

Then, take all this information with you to the dealership and see if the staff there can meet or beat the rate you’ve been given. Dealers often have access to lower, wholesale rates, but they also tack on something to every loan they secure for customers. It’s like The Sopranos: everybody wants a taste.

So, maybe your dealer can secure a 3.5% interest loan–better than the 4.0% you’ve gotten from your own bank. But by the time the dealer adds on her 1% markup, you’re looking at 4.5%. Not so great now, is it? You can try to look for title loans if this kind of situation comes up, as it could help immensely.

You can haggle with your dealer, if that’s your thing. Maybe you can get the rate down, or maybe not. All I’m saying is that if you don’t go prepared, you’ll never know.

One last point about financing: be patient. It can be a long, drawn-out process, with a lot of waiting for your salesperson “to speak with the finance office” (translation: “to get another cup of coffee and chat with her coworkers”). You might be tempted to cut to the chase and sign your life away out of frustration, but keep a cool head, and you might save big over the life of your loan, but don’t forget defaulting on your loan could result in repossession of your car.

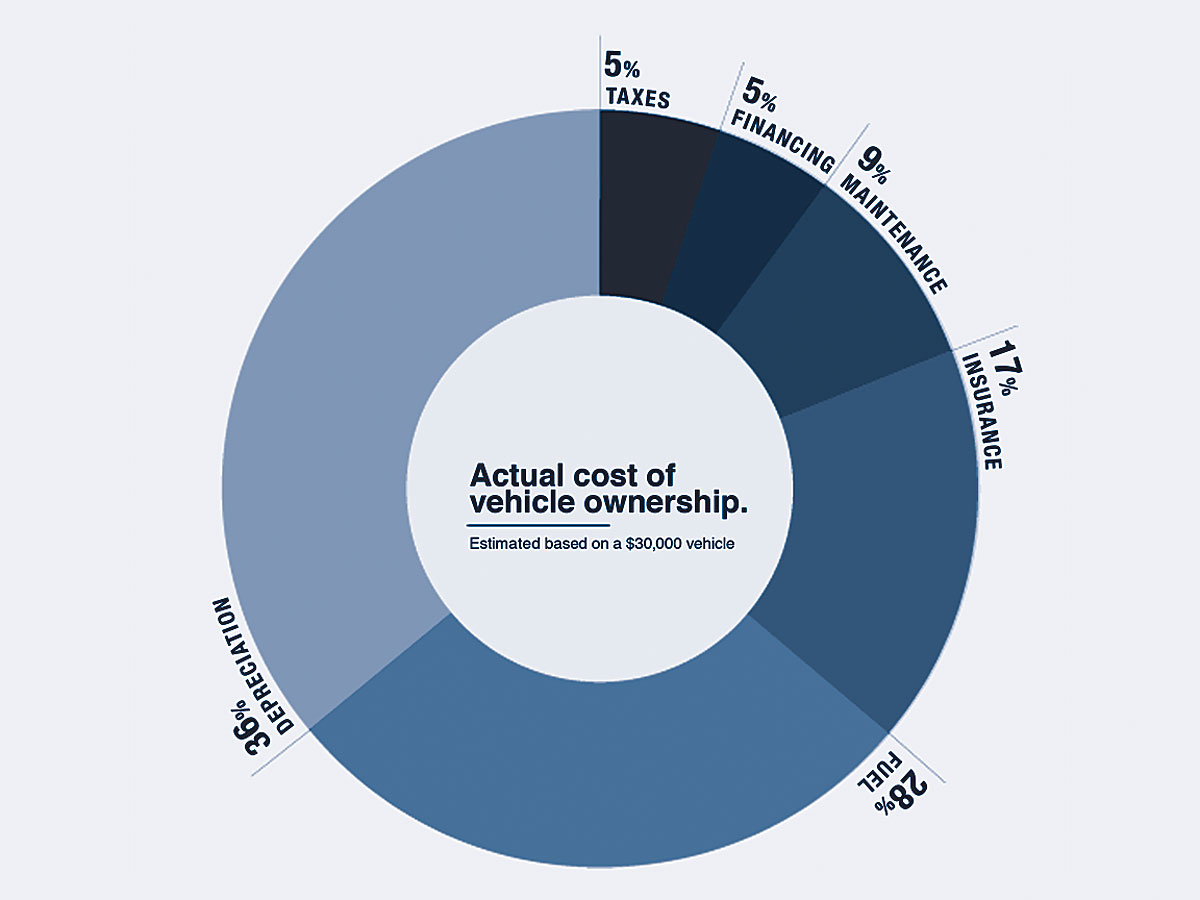

The costs of ownership

Buying a car is an expensive proposition, but owning one is costly, too. It means more than just making monthly payments on your auto loan, it also means paying for insurance, fuel, maintenance, registration, and a host of other things.

Buying a car is an expensive proposition, but owning one is costly, too. It means more than just making monthly payments on your auto loan, it also means paying for insurance, fuel, maintenance, registration, and a host of other things.

Insurance can be particularly expensive, depending on where you live, how old you are, and what kind of car you’re purchasing. For example, a young driver with a sportscar in a state with a high rate of uninsured motorists better have a spotless driving record or they’re going to pay significantly more in premiums than a middle-aged driver with a midsize sedan in a state where everyone ponies up. Across America, the average cost of insurance is around $1,300 per year–though it could be far less or far more, depending on your ZIP code.

If you already have an auto policy, call your insurance agency before you buy your next car and ask for a quote. If you don’t, it’s time to start shopping. There are lots of different quote providers around so check out more about InsurAcar quotes provider to begin with and see if you get any good quotes from there. Remember: most dealerships won’t allow you to roll off the lot without proof of insurance.

You can get a better idea of how expensive your new ride is really going to be by using a cost of ownership calculator. This one from Edmunds employs loads of accumulated data and can estimate certain expenses based on where you live, including fuel, insurance, and depreciation. (As we discussed way back in part one of this guide, depreciation is a real downer, particularly for brand-new cars.) This calculator from NerdWallet requires you to do more of the guesstimating, but it’s useful for older vehicles, since the Edmunds calculator only goes back about six model years.

You’re almost ready to buy that new car! Stick around for our final installment of the Gaywheels car-buying guide, where we’ll give you some parting advice and a quick worksheet to help you find the best vehicle for your lifestyle.